Introduction

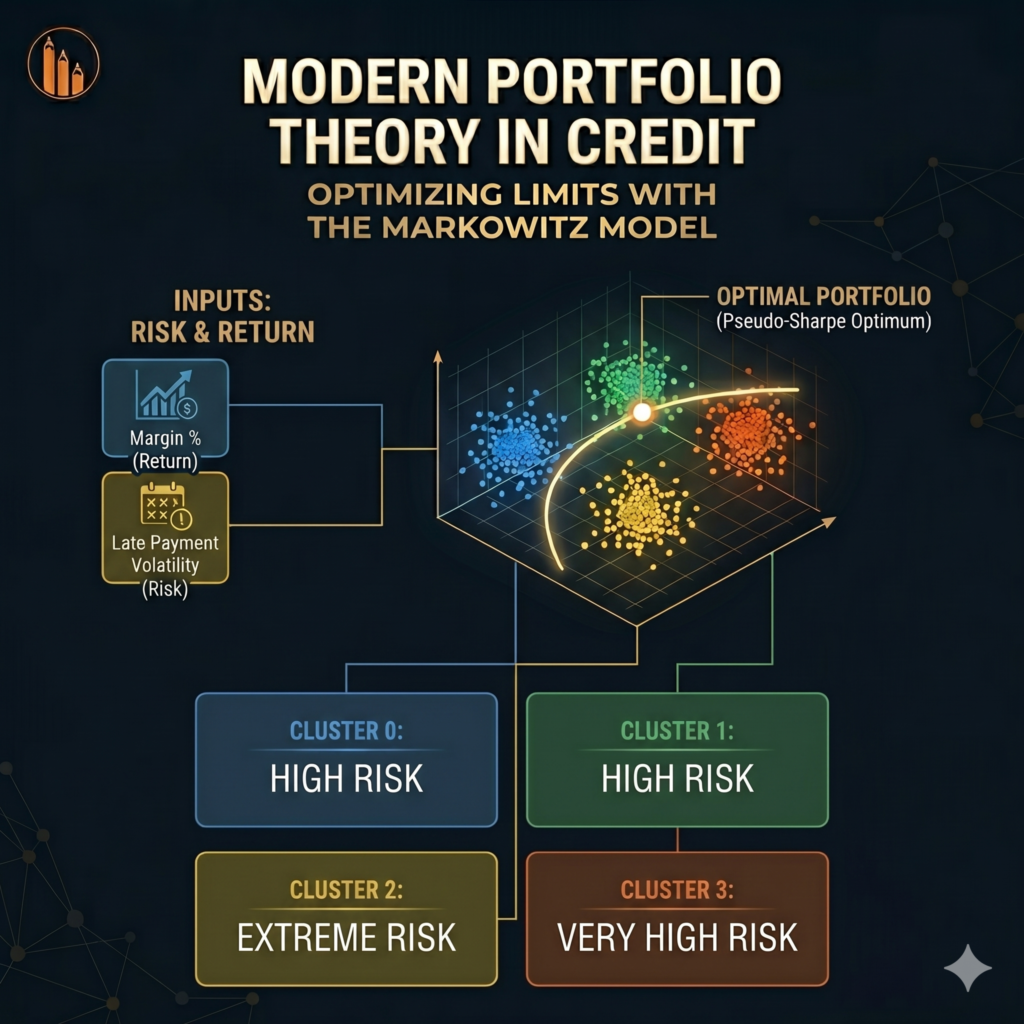

When we think of the “Markowitz Model” or Modern Portfolio Theory (MPT), we usually think of asset management and Wall Street—balancing a stock portfolio to maximize returns for a given level of risk. However, the exact same mathematical principles can completely revolutionize B2B Credit Risk Management.

Instead of stocks, our “assets” are our customer segments. The “return” is the profit margin those customers generate, and the “risk” is the volatility of their late payments or probability of default. By treating credit limits as an investment allocation, we can find the mathematically optimal way to distribute credit across the portfolio.

How It Helps Manage Credit Risk

Traditional credit management often issues limits based solely on a customer’s individual financials. It often ignores the correlation and overall balance of the portfolio. The Markowitz Optimization model solves this by looking at the portfolio holistically.

If we know the Expected Return (Margin) and the Risk (Late Payment Volatility) of our various customer clusters, the algorithm calculates the Efficient Frontier. It tells us exactly what percentage of our total credit exposure should be allocated to each segment to maximize total margin without taking on unacceptable levels of default risk.

The Outcome & Insights

We fed our 4 behavioral segments into the Markowitz optimizer to maximize the pseudo-Sharpe ratio. The algorithm calculated the following Optimal Allocation Weights:

Cluster 0 (High Margin, High Risk Volatility): Allocated 38.8% of total credit limits.

Cluster 1 (Moderate Margin, High Risk): Allocated 25.1% of total credit limits.

Cluster 3 (High Margin, Very High Risk): Allocated 31.0% of total credit limits.

Cluster 2 (Low Margin, Extreme Risk Volatility): Allocated exactly 5.0% (the minimum bound). The algorithm successfully restricted this segment as tightly as possible.

Actionable Takeaway

Under this optimal allocation, the portfolio is projected to yield an 18.77% expected margin while constraining volatility. This proves that credit limits are not just reactive safety rails—they are strategic tools that can be optimized to drive maximum corporate profitability.