Introduction

Credit risk management is inherently forward-looking. While historical metrics tell us how the portfolio performed in the past, they do not prepare us for severe macroeconomic shocks. If an economic downturn hits and average payment delays spike, do we know exactly how much cash flow is at risk?

To answer this, we turn to stochastic modeling—specifically, Monte Carlo Simulations. This advanced statistical technique allows us to test the resilience of our portfolio against thousands of possible future scenarios, providing a clear mathematical boundary for our worst-case risk.

How It Helps Manage Credit Risk

A deterministic forecast is limited. A probabilistic Monte Carlo simulation says: “We ran 10,000 different future scenarios based on the historical volatility of our customers’ payments. Here is the exact probability distribution of our potential losses.”

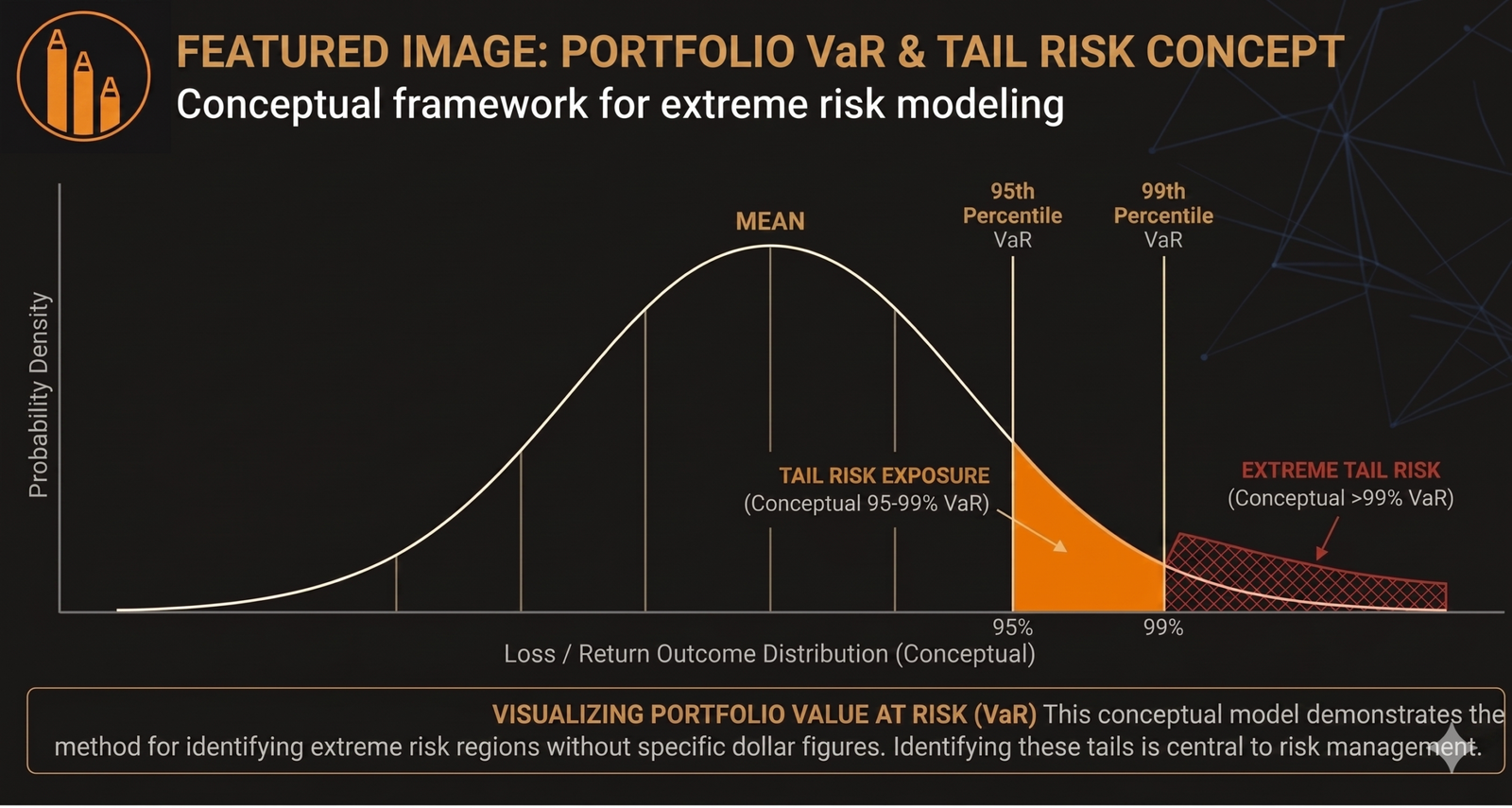

By factoring in the base default rate and the historical standard deviation of late payments, the simulation calculates the Expected Loss (EL) and, crucially, the Value at Risk (VaR). VaR tells management exactly how much capital needs to be reserved to survive extreme events.

The Outcome & Insights

We ran 10,000 simulated 1-year scenarios against a $6.2 Billion portfolio exposure. The results provided clear, actionable risk boundaries:

Mean Expected Loss: $239.6 Million. The baseline cost of doing business.

95% Value at Risk (VaR): $334.3 Million. 95% confidence that losses will not exceed this level.

99% Value at Risk (VaR): $373.5 Million. The extreme “tail risk” exposure.

Actionable Takeaway

By defining a $373M VaR at the 99% confidence level, the finance department knows exactly how much liquidity buffer is required to ensure solvency. Monte Carlo transitions risk management from reactive fire-fighting into proactive capital planning.