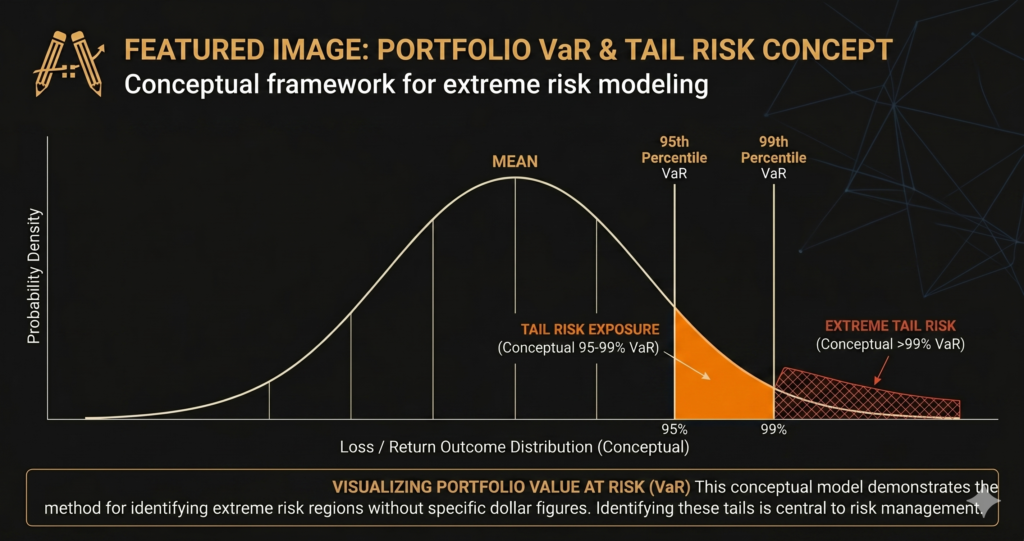

Preparing for the Unknown: Stress Testing Credit Portfolios with Monte Carlo Simulations

Historical metrics tell us what happened; stochastic modeling tells us what could happen. Using Monte Carlo simulations, we stress-tested a $6.2 Billion portfolio against 10,000 macroeconomic shock scenarios to define a precise Value at Risk (VaR). This is how risk management evolves from reactive firefighting to proactive capital planning.